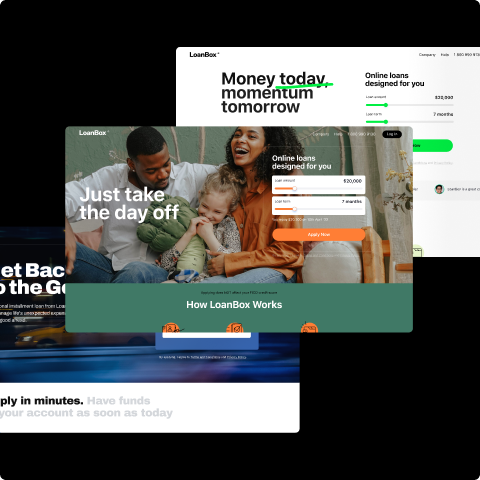

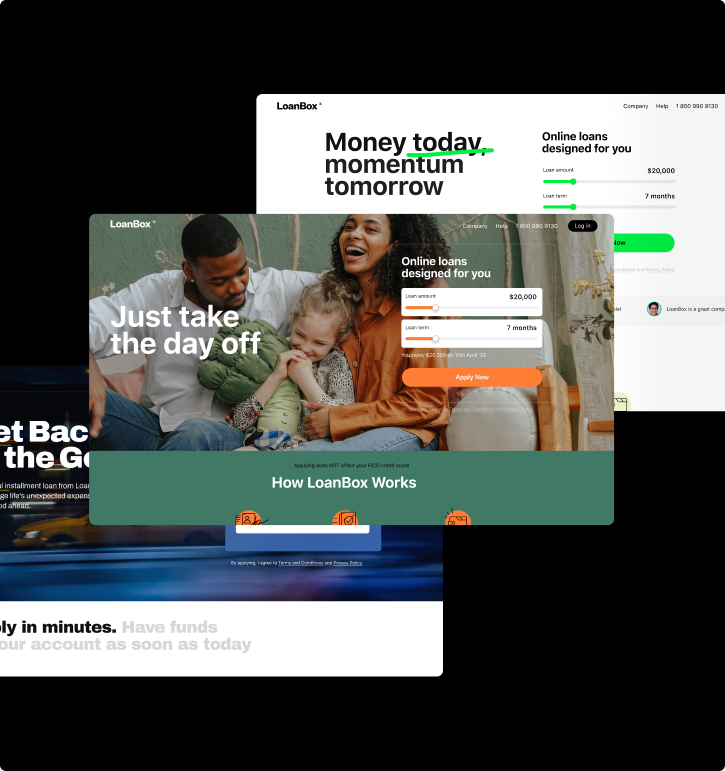

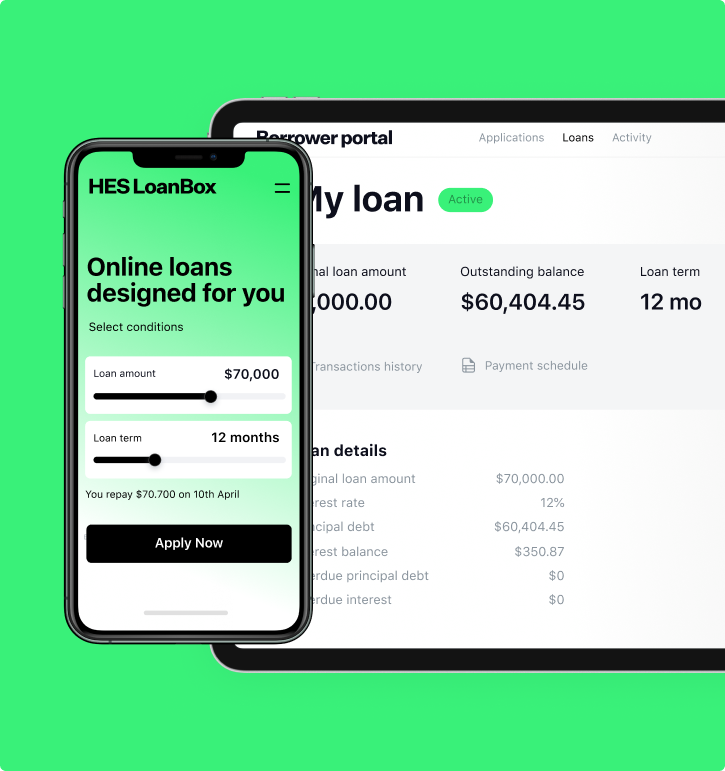

Free landing website

Boost your loan applications through a lending website,

tailored

to your brand identity

Claim now

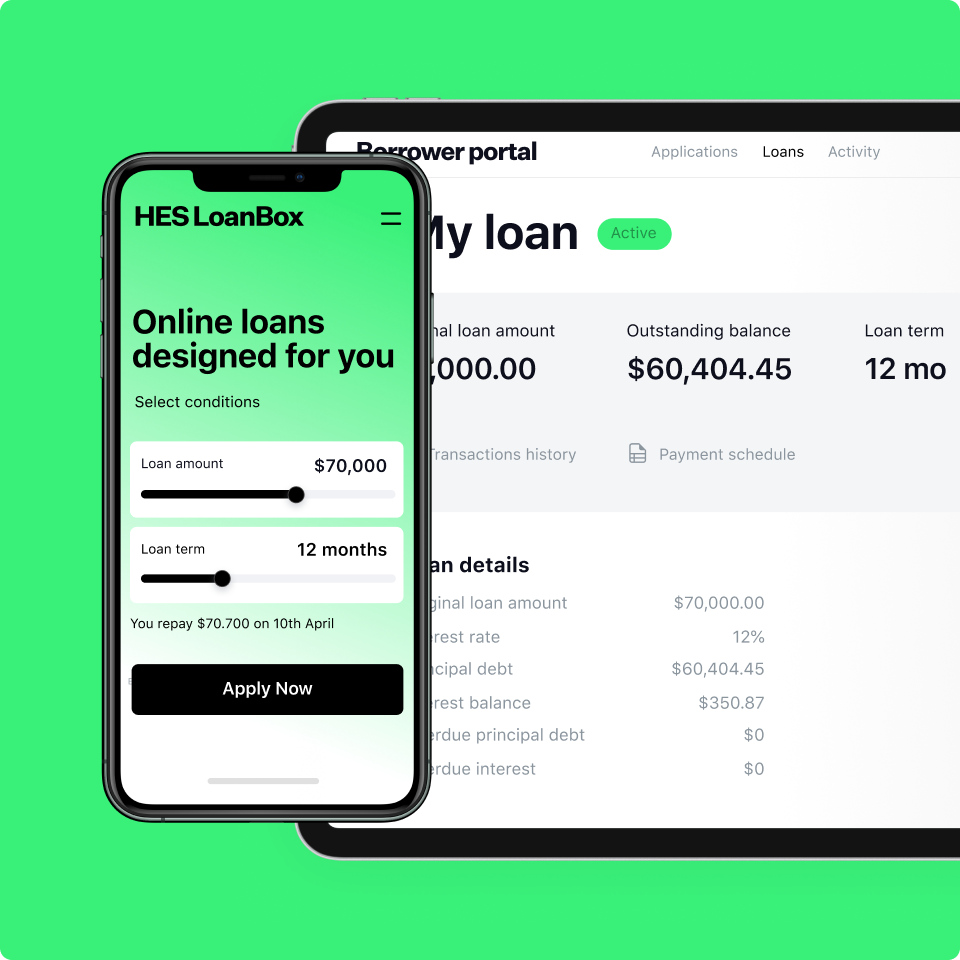

Free HES LoanBox usage

Implement now and use our software for free for the

first 3 months

of the adoption period

Claim now Bootstrapping hypercare

Get 32 hours of free business analyst support to launch

your

digital lending business

Claim now